The Fundamentals of Derivative Pricing for Proprietary Traders

- November 3, 2024

- Posted by: Drglenbrown1

- Category: Derivatives Trading

Understanding the principles and models behind derivative pricing is essential for proprietary traders seeking to optimize their strategies and manage risk effectively.

Derivatives are powerful financial instruments that derive their value from an underlying asset, such as stocks, commodities, or interest rates. Properly pricing these instruments is crucial for traders, as it helps in assessing potential profits, managing risks, and making informed trading decisions. This article explores the fundamentals of derivative pricing, focusing on the primary models and concepts that drive the valuation of options, futures, and other derivative products.

What Are Derivatives and Why Is Pricing Important?

Derivatives are contracts whose value is based on the performance of an underlying asset. Common types include options, futures, forwards, and swaps. Accurate derivative pricing allows traders to:

- Assess Fair Value: By knowing the correct price, traders avoid overpaying and capitalize on undervalued opportunities.

- Control Risk: Proper pricing helps traders manage potential losses by understanding the factors that drive derivative value.

- Optimize Strategy: Derivative pricing provides insights into market expectations, volatility, and potential price movements.

Key Factors in Derivative Pricing

- Underlying Asset Price: The current price of the underlying asset (such as a stock or commodity) directly impacts the value of derivatives.

- Strike Price: For options, the strike price is the agreed-upon price at which the option holder can buy (or sell) the underlying asset.

- Time to Expiration: Derivatives lose value as they approach expiration, a concept known as time decay, especially for options.

- Volatility: Higher volatility generally increases the price of options, as there’s a greater chance of price movement that could benefit the option holder.

- Interest Rates: For forward and futures contracts, interest rates influence the cost of carrying the underlying asset, impacting the derivative’s price.

- Dividends: For stock options, expected dividends can reduce the price of call options while increasing put options due to the effect on the underlying stock’s price.

The Black-Scholes Model: A Cornerstone of Option Pricing

The Black-Scholes model, developed in 1973, remains one of the most widely used methods for pricing European-style options. Based on the assumptions of constant volatility and interest rates, the Black-Scholes formula calculates the fair value of an option using factors like the underlying asset price, strike price, time to expiration, volatility, and the risk-free interest rate.

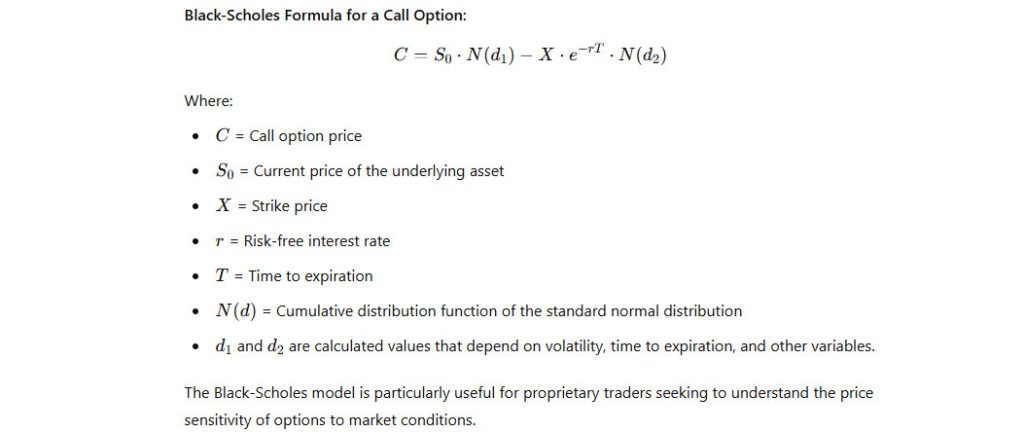

Black-Scholes Formula for a Call Option:

The Black-Scholes model is particularly useful for proprietary traders seeking to understand the price sensitivity of options to market conditions.

The Binomial Option Pricing Model

For options with American-style features (which can be exercised before expiration), the Binomial Option Pricing Model is preferred over Black-Scholes. This model calculates possible future values of the underlying asset in a binomial tree structure, considering up and down movements over multiple time intervals.

Advantages of the Binomial Model:

- Flexibility: Suitable for pricing American options, where early exercise is possible.

- Precision: Allows adjustments for varying volatility and interest rates over time.

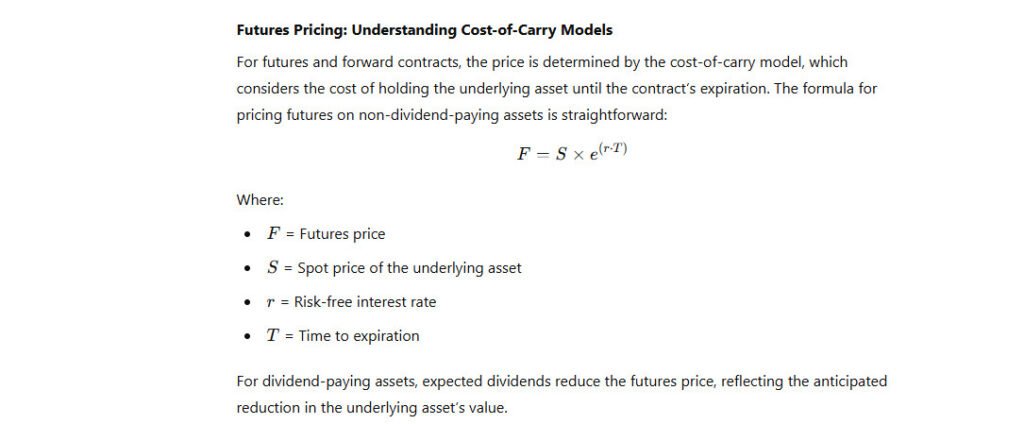

Futures Pricing: Understanding Cost-of-Carry Models

For futures and forward contracts, the price is determined by the cost-of-carry model, which considers the cost of holding the underlying asset until the contract’s expiration.

For dividend-paying assets, expected dividends reduce the futures price, reflecting the anticipated reduction in the underlying asset’s value.

The Greeks: Managing Sensitivities in Derivative Pricing

Proprietary traders rely on “The Greeks” to measure the sensitivity of an option’s price to various factors. Key Greeks include:

- Delta: Measures the option price sensitivity to changes in the underlying asset price.

- Gamma: Indicates the rate of change in Delta, offering insight into option stability.

- Vega: Reflects sensitivity to volatility, a crucial metric for options during market uncertainty.

- Theta: Represents time decay, showing how an option’s value erodes as expiration nears.

- Rho: Measures sensitivity to interest rate changes, important for longer-term options.

Applications of Derivative Pricing in Proprietary Trading

- Hedging Strategies: Properly priced options allow traders to hedge positions in their portfolios, protecting against downside risk.

- Arbitrage Opportunities: Discrepancies in derivative pricing across markets or between similar instruments create arbitrage opportunities for traders.

- Risk Management: By understanding price sensitivity, traders can set stop-loss levels, choose optimal strike prices, and manage their overall exposure.

- Portfolio Diversification: Derivatives add flexibility to trading strategies, allowing traders to benefit from market movements without holding large amounts of capital in the underlying asset.

Conclusion

Mastering derivative pricing is essential for proprietary traders aiming to succeed in a competitive market. By understanding and applying models like Black-Scholes and the Binomial Option Pricing Model, traders can make informed decisions, manage risks, and identify profitable opportunities. The integration of The Greeks and cost-of-carry models further enhances a trader’s ability to navigate the complexities of derivatives.

About the Author

Dr. Glen Brown is a seasoned expert in finance and investments, leading Global Accountancy Institute, Inc., and Global Financial Engineering, Inc. With over 25 years of experience, Dr. Brown combines practical knowledge in proprietary trading, derivative pricing, and risk management, creating advanced educational programs that empower traders.

General Disclaimer

This article is for educational purposes only and does not constitute financial or trading advice. Financial trading involves significant risks, including the potential for loss. Readers should seek independent financial advice before engaging in any trading or investment activities.