66 W Flagler Street, Suite 900, #8535,

Miami, FL 33130, US.

-

The Architecture of Obsession: Sovereign Intellect and Uncompromising Will

- June 9, 2026

- Posted by: Drglenbrown1

- Categories:

No Comments

What happens when high-level intellect meets uncompromising will? Dr. Glen Brown examines obsession not as disorder, but as sovereign concentration — the force that transforms thought into doctrine, doctrine into institution, and institution into legacy.

-

BTCUSD Monthly Zone 5 Test: Bitcoin Structural Hierarchy Analysis by GFE & GAI

- June 8, 2026

- Posted by: Drglenbrown1

- Category: Sovereign Market Intelligence

Bitcoin is testing Monthly Zone 5 while the Weekly Sovereign Baseline has been violated and the Monthly Drift remains positive but compressed. This GFE and GAI analysis explains the structural hierarchy behind BTCUSD’s critical market condition.

-

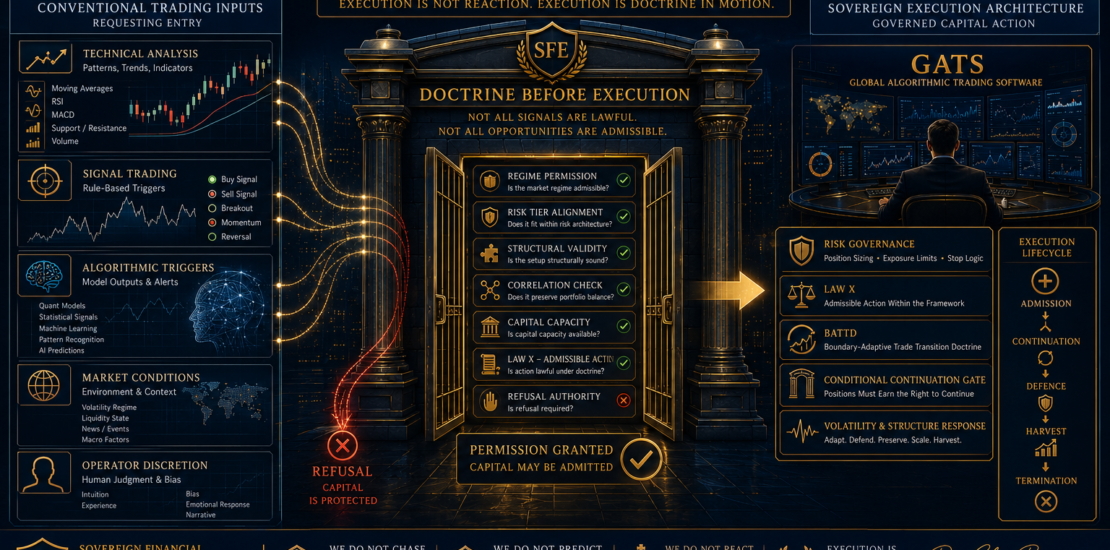

The Engineering of Execution: A Sovereign Engagement with Signal Trading, Algorithmic Execution, and Technical Analysis

- May 9, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

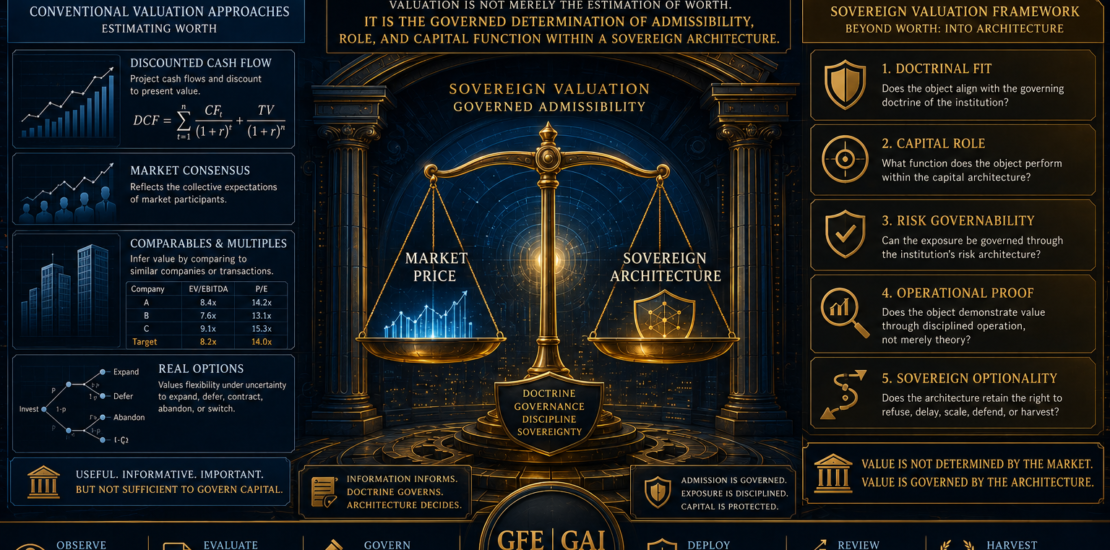

The Engineering of Valuation: A Sovereign Engagement with Discounted Cash Flow, Market Consensus, and Real Options

- May 9, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

The Closed Architecture Principle

- May 8, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

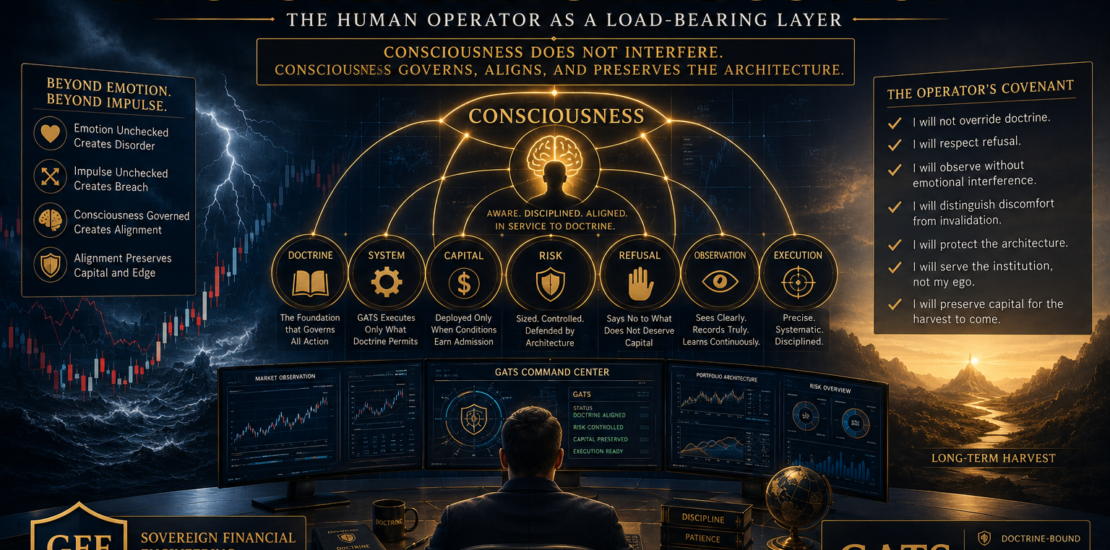

The Role of Consciousness in Systematic Execution

- May 8, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

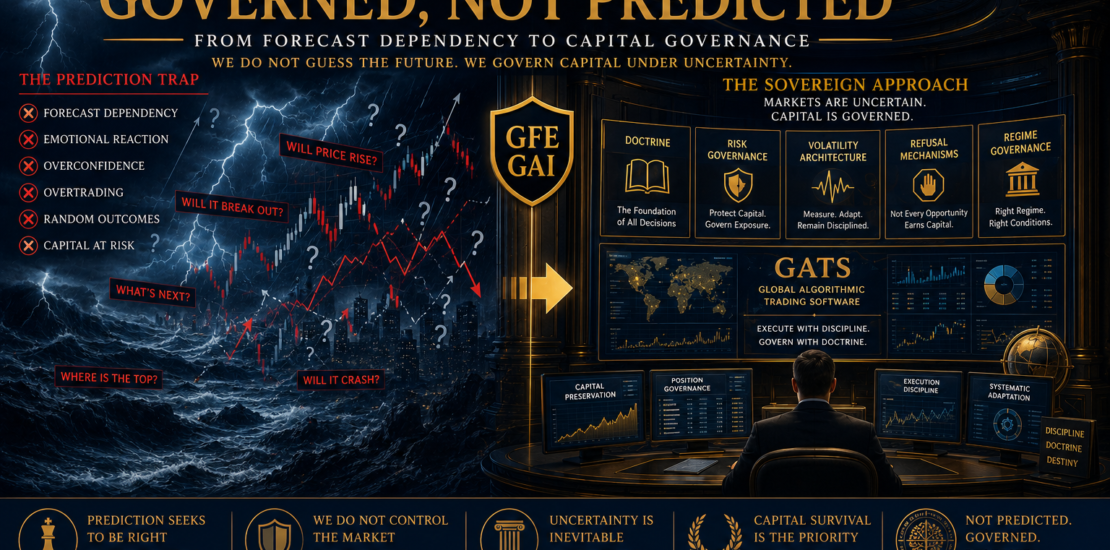

Why Markets Are Governed, Not Predicted

- May 8, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

Why Refusal Is a Capital Function

- May 8, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

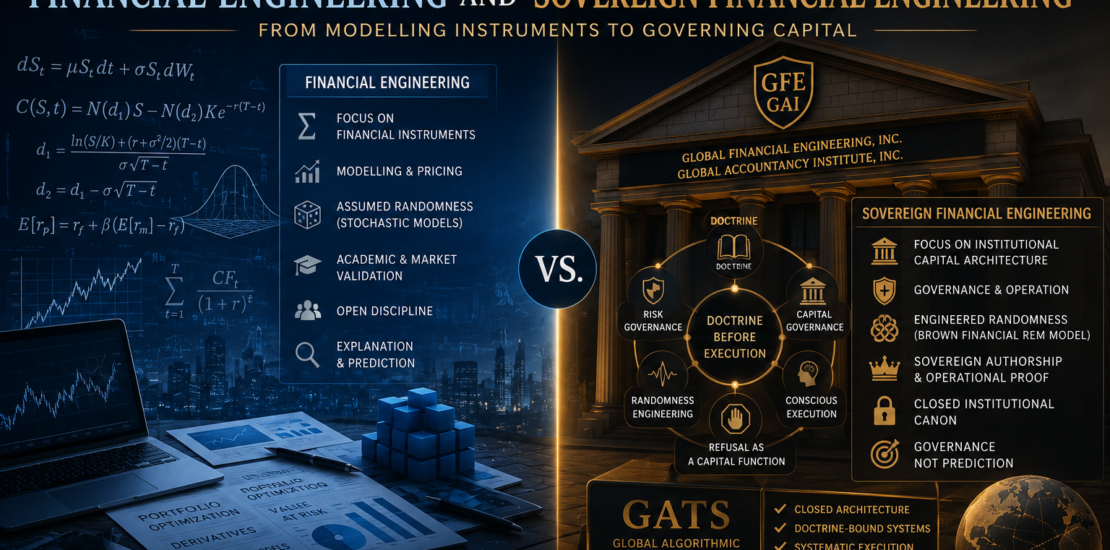

The Difference Between Financial Engineering and Sovereign Financial Engineering

- May 8, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

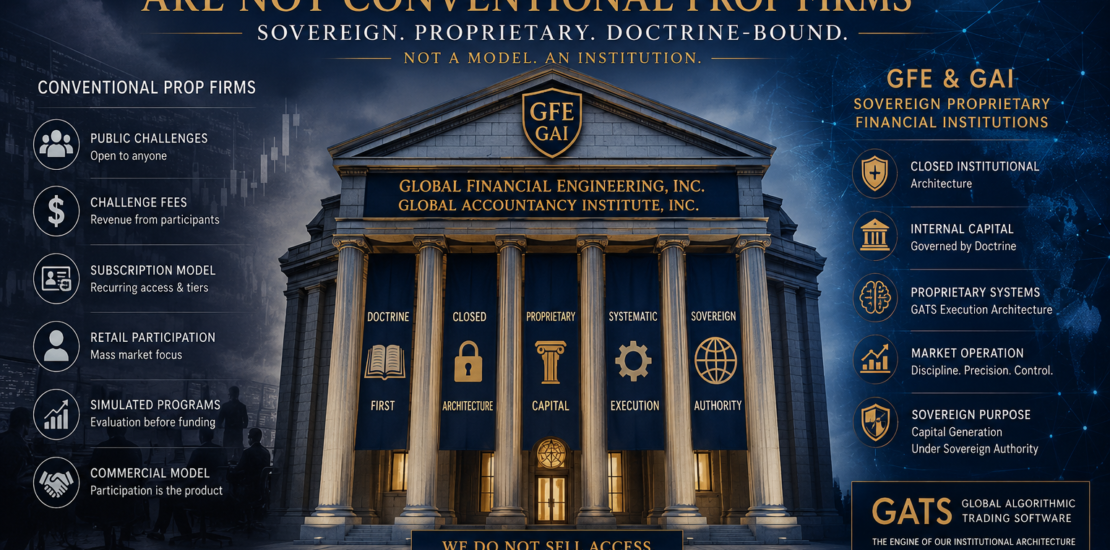

Why GFE and GAI Are Not Conventional Prop Firms

- May 8, 2026

- Posted by: Drglenbrown1

- Category: Core Doctrines & Frameworks

-

What Is Sovereign Financial Engineering? A Public Introduction to the Discipline Founded by Dr. Glen Brown

- May 8, 2026

- Posted by: Drglenbrown1

- Categories:

-

Why Internal Compounding Matters More Than External Fundraising

- March 31, 2026

- Posted by: Drglenbrown1

- Categories: GCPIAUT–GATS Doctrine Series, Proprietary Trading Doctrine

GFE and GAI argue that internal compounding is a higher and more sovereign path to proprietary growth than external fundraising because it proves doctrine, strengthens reserves, and preserves institutional identity.

-

The Instruments Matter: Why Absolute Capacity Requires Absolute Precision

- March 30, 2026

- Posted by: Drglenbrown1

- Category: Proprietary Trading Doctrine

Discover why instruments are not interchangeable in trading and how precision in selection defines true capacity in institutional proprietary systems.

-

The Five-Trust Model: Segregating Asset Classes with Discipline

- March 30, 2026

- Posted by: Drglenbrown1

- Category: Proprietary Trading Doctrine

The Five-Trust Model shows why serious proprietary institutions should segregate asset classes through ring-fenced capital bodies rather than rely on one blended exposure pool.

-

The 252-Slot Doctrine: Rethinking Strategy Capacity in Proprietary Trading

- March 30, 2026

- Posted by: Drglenbrown1

- Category: Proprietary Trading Doctrine

The 252-Slot Doctrine reframes proprietary trading capacity by structuring the strategic field through a defined matrix of instruments, strategies, and governed capital channels.

-

Risk Management Solutions for Proprietary Trading Firms

- March 30, 2026

- Posted by: Drglenbrown1

- Category: Proprietary Trading Doctrine

Risk management in proprietary trading should go beyond trades and include capital governance, reserves, calibration, reporting, and institutional continuity.

-

Why Most Trading Firms Govern Trades but Not Capital

- March 30, 2026

- Posted by: Drglenbrown1

- Category: Proprietary Trading Doctrine

Many firms govern trades with discipline but leave capital under-structured. GFE and GAI argue that true proprietary strength begins with capital governance, not only trade control.

-

Reserve-First Trading: A Different Philosophy of Survival

- March 28, 2026

- Posted by: Drglenbrown1

- Category: Proprietary Trading Doctrine

Reserve-First Trading is the philosophy that proprietary capital should be protected, structured, and preserved through reserves before it is aggressively deployed into markets.

- 1

- 2